![]() So the home buyer and property investor show has been doing the rounds in Australia this year and heads to Melbourne from August 29-31. Whilst it may not be everyone’s idea of an amazing weekend activity, if you’re eager to learn more about property investment and hear from a range of experts it’s a great opportunity. There are a variety of seminars over the three days that cover topics from mortgages and finance through to depreciation and renovations. And at $18 for an online ticket it just might be some of the best money that you can invest!

So the home buyer and property investor show has been doing the rounds in Australia this year and heads to Melbourne from August 29-31. Whilst it may not be everyone’s idea of an amazing weekend activity, if you’re eager to learn more about property investment and hear from a range of experts it’s a great opportunity. There are a variety of seminars over the three days that cover topics from mortgages and finance through to depreciation and renovations. And at $18 for an online ticket it just might be some of the best money that you can invest!

planning

Exciting news!

In the interests of blatant self promotion I’ve attached the following image…more news to come soon!

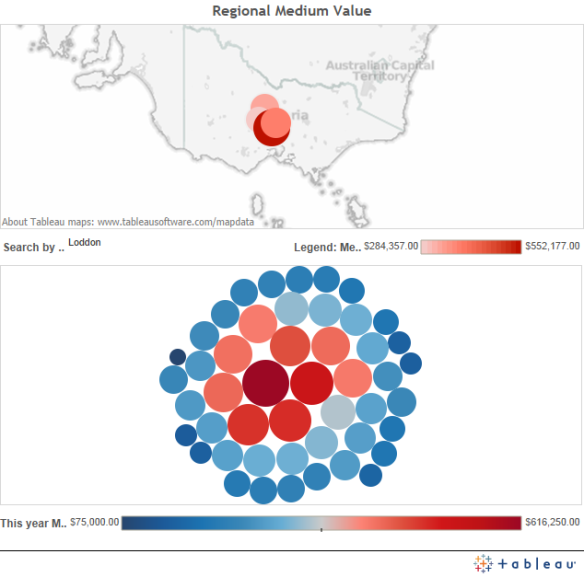

Regional Property Prices

As you may have picked up I’m passionate about regional investment and it forms a large part of my portfolio. A lot of people are skeptical about regional investment and subsequently limit themselves to capital cities. Whilst capital cities have often shown better capital growth than some regional areas there are also some great reasons to consider investing outside of metropolitan areas, not the least of which is that it’s commonly a lot less expensive to get into the market. I have heard many people comment about how expensive it is to purchase in capital cities and that sometimes it’s next to impossible, however in the same breath you’ll hear them comment that regional cities don’t return the same capital growth, so what do they do? Nothing!

As you may have picked up I’m passionate about regional investment and it forms a large part of my portfolio. A lot of people are skeptical about regional investment and subsequently limit themselves to capital cities. Whilst capital cities have often shown better capital growth than some regional areas there are also some great reasons to consider investing outside of metropolitan areas, not the least of which is that it’s commonly a lot less expensive to get into the market. I have heard many people comment about how expensive it is to purchase in capital cities and that sometimes it’s next to impossible, however in the same breath you’ll hear them comment that regional cities don’t return the same capital growth, so what do they do? Nothing!

It’s important to do your homework and weigh up the pros and cons before you limit yourself to just one market which can potentially mean you end up doing nothing and waiting for the prices to drop (it might never happen!). Today I came across the data below which provides the median (not medium as written!) value of a large range of Victorian towns and cities. Information like this can be difficult to come across so it’s good when you can find it. Click on the image below to be taken to the active site. There you can also select and search by region.

Doing the sums #2

I had some great responses to my post on October 13th about doing the sums when looking at investment properties and how important (and sometimes surprising) it is to get an idea of how much it will cost you to start and also to maintain. I’m always keeping an eye out for great examples so will post them when I come across something which shows a simple and affordable approach.

This property is a simple one bedroom unit in a complex of 12 units. It’s in a well established suburban area which is well regarded and in the same city as my first example. The area again demonstrates good infrastructure and is close to necessary facilities (shops, hospitals, schools etc).

On face value the unit appears to be well maintained but of course you would want to inspect not only the property itself but also look around the complex and the units around it. It is for sale for $142,500 and is returning a healthy $190/week. Let’s say that it ticks the boxes as far as the quality and standard of the complex and we manage to get a realistic offer of $140k accepted. What do the figures look like and is it affordable?

| How Much Will It Cost Me? | ||

| Property Price – $140,000 | Deposit (10%) – $14000 | Mortgage – $126,000 |

| Stamp Duty – $3470 | Interest Rate – 4.69% | |

| Conveyancing – $800 | ||

| Mortgage Insurance – $1800 | ||

| Total Costs (estimated) | $20070 |

Once again, these are the main costs with a deposit of 10%, if you can get to 20% for a deposit the mortgage insurance disappears and the total estimated cost would then be $32,270. So you could get this property for an initial outlay of between $20,070 and $32,270. This is all great but let’s once again look at how you maintain this. Rather than being overly conservative, this time I’ve gone with one of the better interest rates that I can find at the moment of 4.69%

| How Much Will It Cost To Service? | ||

| Loan Amount – $126,000/$112,000 |

Council Rates – $900 | Rent Income – $190/wk |

| Interest Rate – 4.69% | Water Rates – $900 | |

| Repayments/Wk (10% deposit) – $150.50 |

Body Corp – $800 | |

| Repayments/Wk (20% deposit) – $134.00 |

Property Mgmt. – $700 | |

| Yearly Repayments – $7826/6968 | Yearly Costs – $3300 | Rent/Yr – $9880 |

For a 1 bedroom unit the rent is very good and in a tight rental market this is becoming increasingly realistic. If you started with the 10% deposit you would find yourself out of pocket $1246 a year (or $24 a week). If you managed to pull together the 20% deposit you would be out of pocket $388 a year or less than $7.50 a week! A dollar a day really is loose change! Come tax time and factoring in some depreciation I’d think it could even be likely to end up being cost neutral.

Again remember this is a ‘one moment in time’ scenario and things can change, but even with some unforeseen expenses and the odd maintenance request a property like this has the potential to be a great starter for an investment portfolio!

Taking your first step – Doing the sums!

I was reading recently that less than 8% of the Australian population are property investors which equates to about 1.8 million people. Of these, the Australian Tax Office reported that 72% of these investors (or around 1.3 million) own just one property. There is a steep drop to less than 100,000 people that own more than 3 properties and less than 1% of Australian property investors (about 15,000 people in the entire country) own more than 6 properties. This information not only shows how few people manage to develop a large property portfolio but also that there is a huge proportion of people that never even get their foot on the ladder. Of course property investing is not everyone’s cup of tea but I have spoken with many people just wanting to make a start but possibly not feeling prepared to take the leap of faith. Today I was speaking with a family member who was interested in learning more about the steps to take to get on the investment ladder. I mapped out a basic example of what I would consider a great ‘starter’, something quite similar to what I started with on my first investment and also an investment which won’t break the bank to get you started. Let’s take a look.

The property I chose to demonstrate with was a one bedroom unit currently for sale in a regional city of around 100,000 people. It is serviced well with good infrastructure and is close to necessary facilities (shops, hospitals, schools etc). The location is highly desirable and the unit itself appears to be in excellent condition. It is for sale for $145k – $155k. Let’s say that we manage to get an offer of $145k accepted, what do the figures look like and is it affordable?

The property I chose to demonstrate with was a one bedroom unit currently for sale in a regional city of around 100,000 people. It is serviced well with good infrastructure and is close to necessary facilities (shops, hospitals, schools etc). The location is highly desirable and the unit itself appears to be in excellent condition. It is for sale for $145k – $155k. Let’s say that we manage to get an offer of $145k accepted, what do the figures look like and is it affordable?

| How Much Will It Cost Me? | ||

| Property Price – $145,000 | Deposit (10%) – $14500 | Mortgage – $130500 |

| Stamp Duty – $3700 | Interest Rate – 5.5% | |

| Conveyancing – $800 | ||

| Mortgage Insurance – $1800 | ||

| Total Costs (estimated) | $20800 |

These are the main costs with a deposit of 10%, if you can get to 20% for a deposit the mortgage insurance disappears and the total estimated cost would then be $33,500. So you could get the property for an initial outlay of between $20,800 and $33,500 but what then? How are you going to service the loan and how much is it going to cost out of your own pocket?

| How Much Will It Cost To Service? | ||

| Loan Amount – $130,500 | Council Rates – $900 | Rent Income – $200/wk |

| Interest Rate – 5.5% | Water Rates – $900 | |

| Weekly Repayments – $171 | Body Corp – $800 | |

| Property Mgmt. – $728 | ||

| Yearly Repayments – $8892 | Yearly Costs – $3328 | Rent/Yr – $10400 |

The rent on this property is very healthy and over the course of the year you would be out of pocket $1820 (or $35 a week). Remember that this is a ‘one moment in time’ scenario and things can change in both positive and negative ways. The interest rate above is fairly conservative currently, I could locate a deal at 4.69% which would reduce your weekly repayments to $156 meaning you’re now only out of pocket $20 a week! If you managed the initial 20% deposit at that interest rate then your repayments drop to $139/week which means you would have to dig between the couch cushions once a week to find the spare $3 to fund your investment property!

On the flip side you also need to be aware that tenants can move out, things can break that need repairing and the cost of rates, insurance and property management can (and usually do) go up. It would be great to only have to pay $3 a week but in reality it will sometimes be more than that. Can I afford $20, $50 or even $100 a week if it came to that? These are all questions that you need to ask yourself and factor into your own budget. Overall though, what I’m hoping is that this example shows that you don’t need to be a millionaire to start on the investment ladder. Yes it takes some saving but it’s property and you don’t get it for free. When you do the sums though it can often work out to be a lot less than you may have initially thought!

Tip 3 – What do you want to achieve?

When considering investing in property it’s essential to think carefully about why you are doing it and why you are choosing to invest in property over any other options. There is a lot of media coverage in many countries about the process and benefits of property investing and it’s certainly encouraging to a lot of people, however there are many questions that you should be asking yourself before heading down that path. One of the things I talk to people a lot about is to be ‘cautiously receptive’ of other people’s advice (including mine as well) and when you start telling people that you are thinking about buying an investment property you’ll be surprised at how many people have an opinion on it and plenty of advice to go along with it.

When considering investing in property it’s essential to think carefully about why you are doing it and why you are choosing to invest in property over any other options. There is a lot of media coverage in many countries about the process and benefits of property investing and it’s certainly encouraging to a lot of people, however there are many questions that you should be asking yourself before heading down that path. One of the things I talk to people a lot about is to be ‘cautiously receptive’ of other people’s advice (including mine as well) and when you start telling people that you are thinking about buying an investment property you’ll be surprised at how many people have an opinion on it and plenty of advice to go along with it.

Ultimately, you are the only one that can decide if it’s the right option for you and your circumstances and this requires every potential investor to hold up a mirror and ask themselves some questions. Here are a few prompts that I found (and still continue) to find useful when considering buying a property for investment.

- What do I want to get out of investing in property? Am I approaching this as a long term investment that I’m happy to maintain for years to come, or am I dong this for some fast returns?

- Am I aiming to establish a portfolio of properties or am I going to buy one property for investment? If I’m aiming for multiples, how do I do that?

- Do I want my investments to eventually be my primary income? Am I aiming to have it as a ‘retirement fund’ or eventually extra spending money?

- Will I be disappointed if it takes a long time for me to see some positive cash flow from my investment? What if it starts off losing money?

- Examining my finances, am I in a position to invest in property…realistically? Have I been putting off investing because I think I may not be able to do it financially?

- Do I want a ‘set and forget’ investment or am I prepared to put time and energy into my investments? I think this question is very important to be able to answer as property can end up being either of those things.

- How much do I know about being a landlord and how much time am I prepared to put into the process of learning about it?

- Am I realistic about how I would manage if something goes wrong? What about if my income drops, if my family circumstances change, if I need to pay for major repairs or if I have issues with a tenant?

These questions are just a starting point for things to think about and all before you have been to an open for inspection. Often the first thing people will do when thinking about property investment is to go looking at properties and quickly fall in love with their dream investment. My view is that this can often be the first mistake in a long line of potentially costly steps. Remember, this is an investment and you need to be clear about what you want to achieve before you find yourself signing a contract of sale! Yes, it’s not the exciting part but it is essential. Being clear about your goals through investment will be one of the best first steps you can take and will certainly help pave the way for a successful journey. Try not to be put off by it, sometimes it’s challenging to put the brakes on and ask yourself such questions and you also need to be prepared to deal with your answers. If you don’t like what the answers are then it means that you need to do some more work before you get out there buying a property. It’s entirely worth it though so persevere!

If you are starting to think about investing or already are, what are the questions that you would recommend? What have you found useful to consider? Add them below!